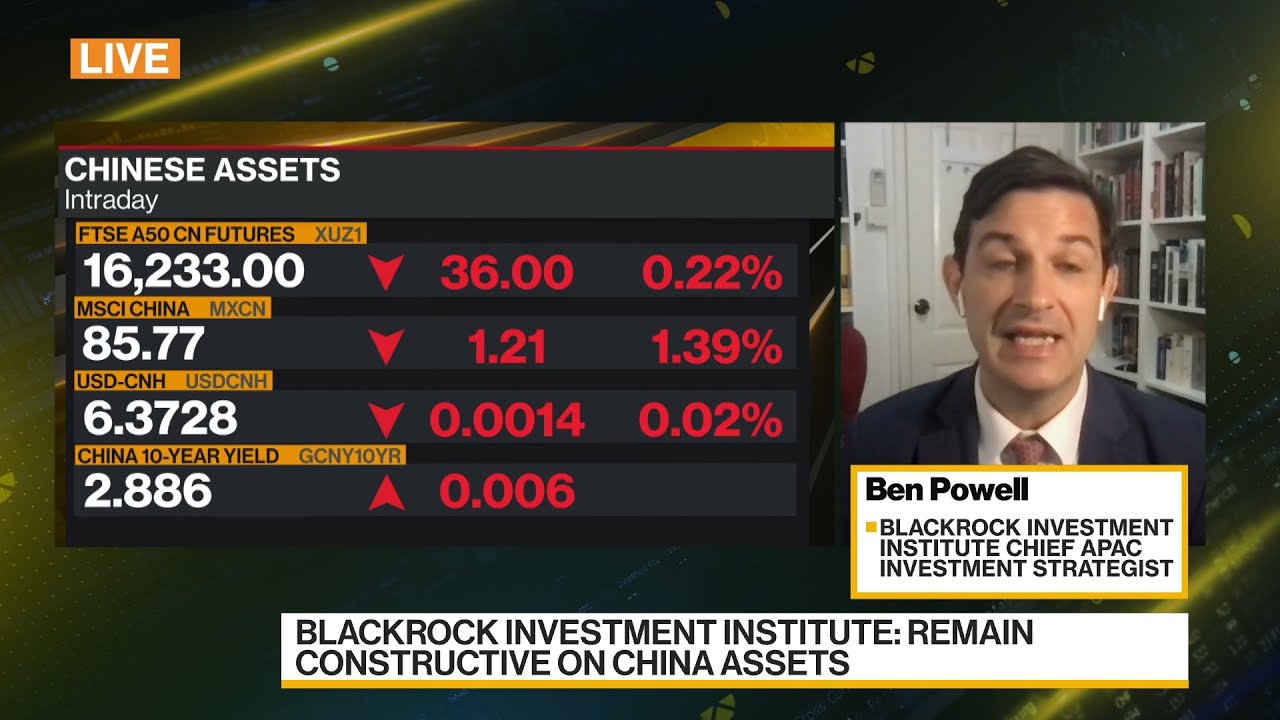

Ben we heard from jay pulaski of tpw Advisory talking about potentially this Being an opportunity for investors Especially when it comes to thematic Trends i know that you're constructive In chinese assets what do you make of The latest Uh good morning so for us at the Blackrock investment institute uh the U.s china tensions are structural In nature and are therefore uh gonna Persist and that's gonna be true for Years to come maybe even decades to come Almost regardless of who happens to be Uh in the white house for example so the Structural nature of the tensions are Real but actually for us in 2022 uh we Think we could see something of a Lessening of the tensions Frankly because both sides both the u.s And china side Are so busy domestically clearly very Important political years both in the U.s With the midterms in q4 and similarly in China are very important political year As we all understand so it seems to us That these tensions are going to persist As i say for years to come that's kind Of the mood music For the foreseeable future however in 22 Actually we think we could see something Of a tempering Just because both sides are so busy

Minding their own stores as it were with Their domestic political calendars uh Where we think we'll see more focus So what do the domestic narratives in China mean for the markets how positive And supportive could that be we have Seen the pboc turn a little bit uh More Easier on monetary policy not to mention That fiscal measures perhaps seem to be A little bit more supportive lately I think so so we at the black rock Investment institute we upgraded china Equities to a small overweight dipping Our toes in On september the 27th and we did that Because we expected to see Increasing signs of a broad based Loosening not just Monetary policy triple r cuts but fiscal And critically Maybe a peaking in the Intensity of some of the regulatory Downdraft that we've seen And so far i think we've seen uh some More evidence in that direction uh Clearly we want to see more but Critically over the last 10 days Politburo meeting economic work Conference i think kind of a huge deal Suggesting that indeed china has pivoted To a more supportive growth supportive Uh policy mix at least tactically uh Over the next six to 12 months and for

Us given how kind of A bearish sentiment is towards china Chinese equities in particular that Combination of quite bearish sentiment And a fundamentally important pivot Towards tactically more growth Supportive uh policies from chinese Authorities uh we think it's Constructive so we remain uh overweight Chinese equity equities uh in our 2022 Outlook and continue to be Somewhat constructive moderately Overweight china equities for some of Those reasons Ben i'm assuming though you have to be Pretty selective with that there's not Only regulatory downdraft but i give you Exhibit a chinese real estate companies Evergrand kaiser now How long do you see these sorts of Issues persisting in china's real estate Sector I think well structurally i think for a Long time i think one of the ambitions For china authorities Is to create a more markets-driven Pricing of risk and to do that you Actually need to have some risk which Means the potential at least For haircuts and bankruptcy and so forth If china can achieve that it should lead To a differentiated cost of capital for Companies with different uh prospects Which would be i think rather

Constructive in terms of the efficiency Of the economy and the market and so Forth so it's going to be very Interesting clearly very delicate and Frankly very hard for authorities but if China can land the plane of Simultaneously defending growth and Keeping its uh high enough to support Employment and social harmony and kind Of simultaneously inject risk risk Pricing into markets Then that to me would be quite a Constructive achievement Both temporarily i guess more of the Short-term stimulus stuff but more Fundamentally if china can move away From the implicit guarantee Towards at the margin a a greater uh Reliance i suppose on markets to Allocate capital and as i say to do that You need to have risk there's just no Way around that uh then that would be uh Actually strategically over the medium Term uh an encouraging thing as china Moves away from setting the price of Risk by uh dig tap towards more of a Market-based uh Pricing of risk and capital allocation Model Is perhaps a less turbulent option japan I know you're bullish on japanese Equities but how do valuations look for You there Japan looks uh yeah pretty attractive we

Think valuations similarly seem Uh relatively undemanding when we look At the equity risk premium that one can Earn as a global investor Japan is uh somewhat outstanding by some Global peers by comparison to some Global peers japan should benefit from The i guess double tailwind of the Global uh reopening Of course we're all watching omicron Very closely uh of course but it seems To us as if the uh the activity restart Will continue to broaden uh through 22 And japan obviously with a fantastic Export uh sector should have some Gearing to that and on the other hand of Course jaman has got its own domestic Activity restart uh which again should Kind of continue through 2022. so when We consider that and the potential for The new uh government to maybe do a bit More than uh i was previously Anticipated in terms of a bit of Stimulus a bit of reform and so forth Then the valuation to your question paul Valuation looks relatively undemanding Set against the backdrop of those Various potential catalysts that we Could see start to play out in the In the months ahead